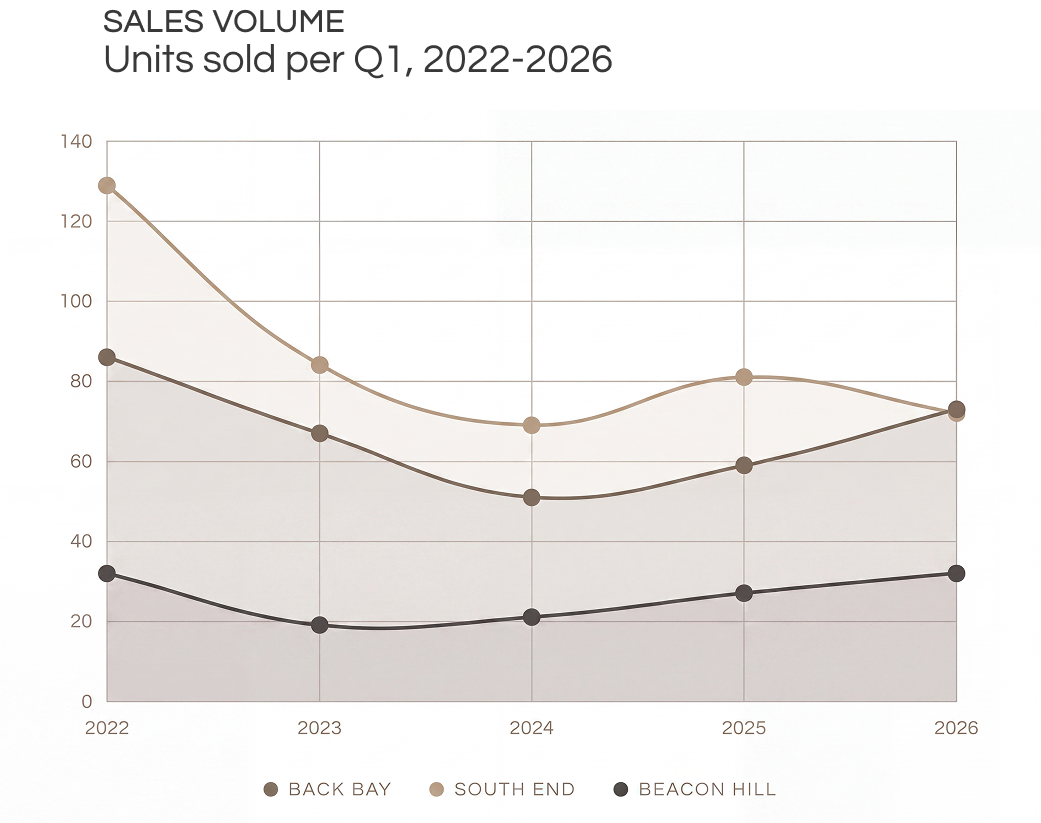

The first quarter of 2026 closed with a number that, on its face, looks like routine variation. Across Back Bay, Beacon Hill, and the South End, sales volume moved in three different directions, up twenty-four percent, up nineteen percent, down eleven percent, and the headlines wrote themselves accordingly.

But the story underneath is a different one. The three neighborhoods are not behaving like three separate markets. They are behaving like three views of the same shift, a quiet bifurcation that is reshaping what gets bought at the top of Boston’s residential market, and what does not.

Every mature market eventually bifurcates. Wine collectors stopped buying mid-tier Bordeaux a decade ago and concentrated their spend on first growths and grower Champagne. The contemporary art market hollowed out the middle in the late 2010s, under-fifty thousand dollar primary works thinned, eight-figure trophies kept setting records. The watch market did the same: entry pieces moved on hype cycles, and unique-piece auction results kept climbing in parallel.

The pattern is consistent. As a category matures, the comfortable middle, the safe, mid-priced, broadly acceptable object, loses its constituency. Buyers who have done their homework migrate toward two ends: the strategic entry point that gives them a foothold, and the irreplaceable object that justifies its price by being singular. Boston’s premium residential market is now showing the same shape.

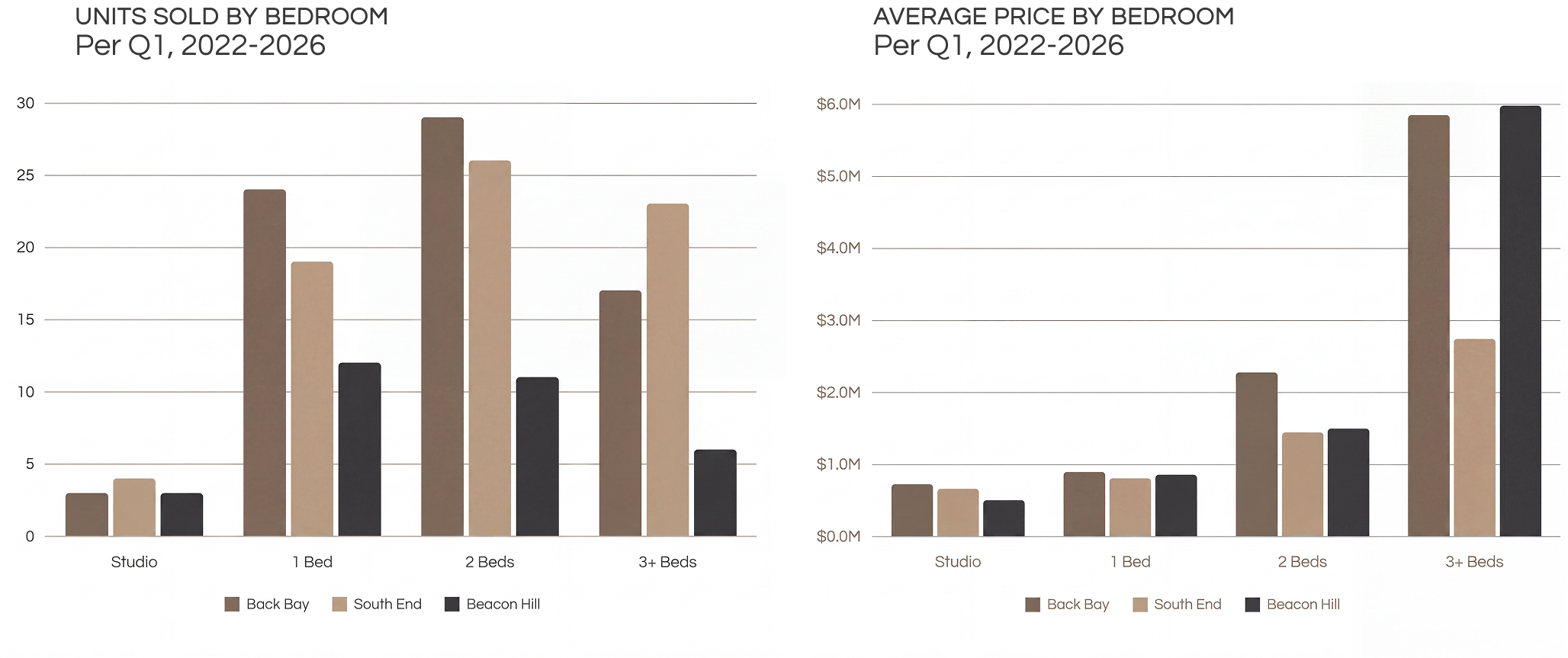

Back Bay posted seventy-three sales in Q1, the strongest first quarter since the post-pandemic peak. The headline number reads as recovery. The composition tells a more specific story.

One-bedroom sales nearly doubled year-over-year, from thirteen to twenty-four. Properties under a thousand square feet accounted for a meaningful share of the volume. The average sale price fell seventeen percent, not because Back Bay is depreciating, but because the buyer profile shifted. The activity is concentrated at the entry point. Decisive buyers are taking positions in the neighborhood at the smallest unit they can credibly own.

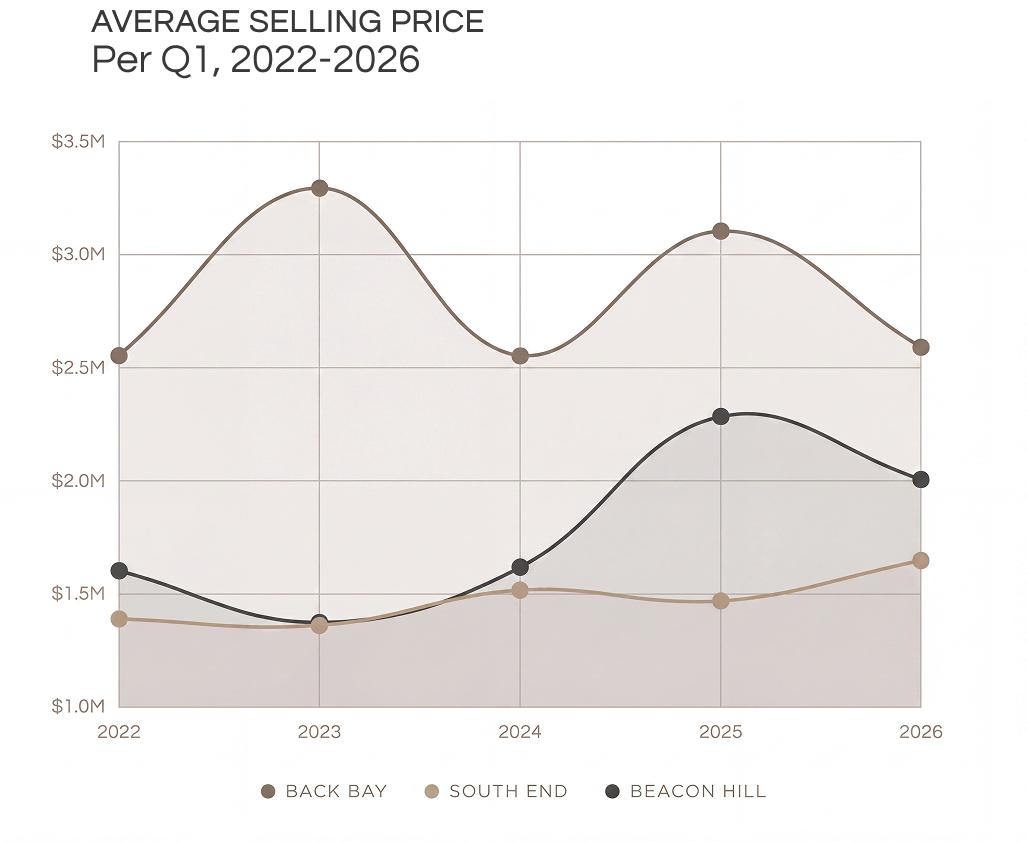

At the same time, the over-2,400-square-foot tier moved eleven units at an average of $7.7 million. The middle (the comfortable two-bedroom in the $1.5 to $2 million range) is where the market thinned.

Beacon Hill’s median sale price fell from $2.2 million in Q1 2025 to $992,000 in Q1 2026, a fifty-five percent drop that, read in isolation, would suggest a neighborhood in retreat. It is not. It is the same bifurcation expressing itself more sharply.

Studio and one-bedroom transactions accounted for fifteen of the thirty-two sales in the quarter, nearly half. One-bedroom volume doubled. Meanwhile, the three-plus-bedroom tier averaged $5.98 million, a fifty-two percent year-over-year increase, with five sales over $5 million. Beacon Hill did not weaken. Its activity migrated to its two ends, and the median moved with the volume.

The South End looks, by volume, like the soft neighborhood of the three, seventy-two sales, down eleven percent. Look one layer deeper and the same pattern appears in a slightly different costume.

Three-plus-bedroom transactions rose fifty-three percent, from fifteen to twenty-three. Price-per-square-foot in the 1,501–1,800 range climbed fourteen percent. The studio segment quadrupled. What softened was the conventional middle — the standard two-bedroom condo that for years was the South End’s default trade. Twenty-six of those sold this quarter, down from forty-one a year ago. The neighborhood did not slow down. It became more selective about what it absorbed.

When a market bifurcates, two things become true at once. The strategic entry (the smaller, well-located, architecturally credible unit) becomes a sharper instrument than it used to be. It is no longer a starter property; it is a position. Buyers under fifty are using it that way: as a foothold in a neighborhood whose larger residences they may grow into later, or never, but whose address compounds quietly either way.

For sellers, this is not a story about pricing. It is a story about positioning. The properties that traded well this quarter were the ones whose argument was specific, provenance, scale, light, architectural lineage. The properties that lingered were the ones whose argument was generic.

For decades, the comfortable middle of the Boston market did most of the work. Today, the work is happening at the edges.